Industry Reports

Tech-Led FDI & Resilient Sectors: Private Market Opportunities in ASEAN

ASEAN’s Divergent Growth

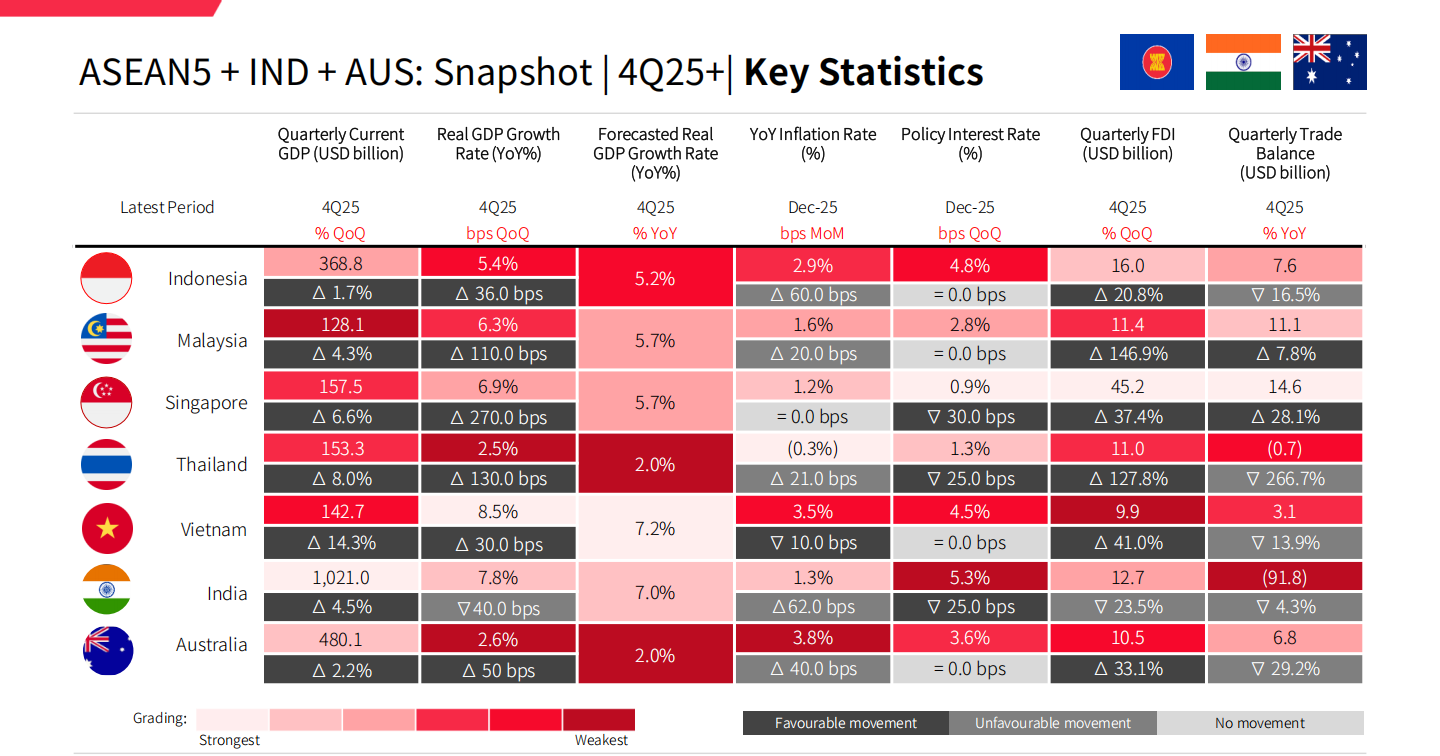

Against a backdrop of divergent growth across Southeast Asia, PE/VC, banks, and M&A advisory firms are sharpening focus on data-driven industry research, actionable company data, and robust deal sourcing platforms to identify high-confidence targets. Speeda’s latest 4Q25 ASEAN5 + India + Australia reports reveal a region undergoing structural transformation: while headline growth varies widely, FDI inflows gained broad momentum across the region, led by sharp rebounds in Singapore, Malaysia, and Thailand, while India’s inflows eased from its 3Q25 peak, with investments increasingly concentrated in higher-value manufacturing, digital infrastructure, and energy-transition projects.

ASEAN economies posted solid year‑on‑year GDP expansion in 4Q25, with Vietnam (8.5%), India (7.8%) and Singapore (6.9%) leading the pack, while Thailand recorded a more moderate 2.5% YoY growth, still exceeding its full‑year 2.0% target. Such divergence reinforces the need for granular industry research rather than blanket regional views. For dealmakers, M&A target screening must prioritize sectors with structural outperformance and shock resistance—traits measurable via consistent company financial data and macro benchmarks.

Selective FDI Flows

FDI flows have become highly selective. Thailand alone saw approved FDI surge 127% quarter‑on‑quarter to USD 11.0 billion in 4Q25, with a remarkable 65% directed into the digital industry, fueled by data centers and cloud infrastructure. Singapore remained the region’s largest FDI destination at USD 45.2 billion, drawing capital into finance, tech, and data services, reinforcing its role as a hub for business investment.

Meanwhile, foreign investment in Vietnam rebounded strongly, with manufacturing and processing attracting the bulk of capital, supporting long‑term industrial upgrading and cross-border deal flow. For investors, this selective FDI landscape means that effective deal sourcing venture capital strategies must map capital flows to sector-specific growth drivers, rather than relying on broad regional assumptions.

Resilient Sector Opportunities

Sector performance is increasingly uneven. Speeda’s shift‑share and stress‑test analysis identifies Thailand’s “shock‑proof core”: digital & ICT, healthcare, wholesale & retail, and water & waste management. These sectors outpace national GDP and remain stable through political, inflation, and trade shocks—critical for benchmark VC strategies and long‑hold portfolios.

Digital infrastructure, in particular, benefits from hyperscaler investments, AI adoption, and supportive regulation, making it a focal point for deal sourcing venture capital teams across ASEAN.

Mastering ASEAN’s Unique Market Dynamics

For investors and advisors, how to value a company in this region requires more than traditional multiples: it demands integrated financial data, sector benchmarks, and policy visibility. Thailand’s supportive tax regime — including corporate income tax relief and targeted incentives for digital and sustainable projects — can enhance cash flows and support higher valuations for eligible firms, alongside other operational and market drivers.

Political and regulatory shifts further shape risk and return. Recent developments also underline the need to incorporate geopolitical and border‑related risks into deal sourcing and due diligence. Singapore’s expansion of digital and green trade agreements strengthens its ecosystem for cross-border ventures.

Leveraging Data to Unlock ASEAN’s Next Wave of Deals

Looking ahead, regional growth remains strong but polarized. Vietnam targets ≥10% full-year GDP and India 7.3% in FY26, while Thailand moderates to 1.5–2.5% and Indonesia holds at mid-5%, widening the gap between export-exposed and domestically driven economies.

Policy rate trajectories are increasingly country-specific: Australia’s RBA reversed course in Jan-26 with rate hikes to address above-target inflation, contrasting with more accommodative stances elsewhere in the region.

Malaysia and Vietnam are likely to remain the region’s brightest FDI spots: Malaysia leverages its semiconductor supply chain position, while Vietnam’s full disbursement of its 2026 public investment plan and 13–15% retail sales growth target signal strong investment-led pipelines ahead.

Overall, 2026 offers upside for firms aligned with high-growth, investment-led markets but will demand more granular, country-specific strategies as growth, policy, and FDI dynamics increasingly diverge across the region.

Join Our Exclusive Webinar to Learn More

Dive deeper into Southeast Asia’s tech-led FDI landscape, resilient sector opportunities, and data-driven deal sourcing strategies. Our expert and guest speaker will equip you with actionable insights to refine your investment playbook for 2026.

Registration Link: https://sea.ub-speeda.com/asean-insights/solutions/event20260508/