Trend Reports

Malaysia’s Semi Strategy: New Deal Opportunities in ASEAN Chip Supply Chains

Private-Dominated Sectors Can Still Be Analyzed Effectively

Searching for Actionable Semiconductor Transactions Beyond Traditional Hubs?

For global and regional investors, Malaysia is no longer just a low-cost “back-end factory” at the margins of the ASEAN semiconductor landscape. Today, the country anchors global chip supply chains with around 13% of worldwide back-end semiconductor manufacturing, underpinned by more than 50 years of assembly, testing and packaging (ATP) expertise and a deep ecosystem of local SMEs supporting multinational chipmakers.

As Malaysia rolls out its National Semiconductor Strategy (NSS), backed by a RM25 billion fiscal package and a clear three-phase roadmap, it is moving decisively up the value chain from back-end production into front-end manufacturing and IC design. That shift is already reshaping ASEAN chip supply chains and opening new deal opportunities for private equity, venture capital, banks, M&A advisors and transfer pricing specialists looking at Malaysia semiconductor exposure.

For dealmakers searching for actionable semiconductor transactions beyond traditional hubs, Malaysia’s combination of industrial strategy, cluster depth and corporate pipelines makes it a core geography for upcoming ASEAN chip investments and M&A.

NSS: A RM25 Billion Fiscal Engine for Malaysia’s Chip Upgrade

Malaysia’s National Semiconductor Strategy is the central policy engine behind this new wave of semiconductor investments. The NSS is backed by a RM25 billion fiscal package that explicitly targets four levers: company growth (~RM11 billion), capital grants (RM10 billion), workforce training (RM2.5 billion) and R&D (RM2 billion). The ambition is to crowd in more than RM500 billion of investments in advanced packaging, IC design and manufacturing equipment, including new wafer fabrication and equipment FDI.

Under a three-phase roadmap, Malaysia aims to first scale and modernise its OSAT base, then expand wafer fabrication capacity and power semiconductor production, and finally cultivate domestic champions in IC design, advanced packaging and equipment. By 2030, the NSS targets more than 100 new IC companies with RM1 billion in annual revenue and at least 10 local design and advanced packaging players earning between RM1–4.7 billion each.

For investors, this is effectively a publicly supported pipeline of potential future acquisition targets, growth equity deals and project finance mandates across the semiconductor value chain. For banks and M&A advisors, the fiscal incentives and grants improve project IRR, support higher leverage and de-risk large capex decisions in fabs, OSAT expansions and equipment facilities.

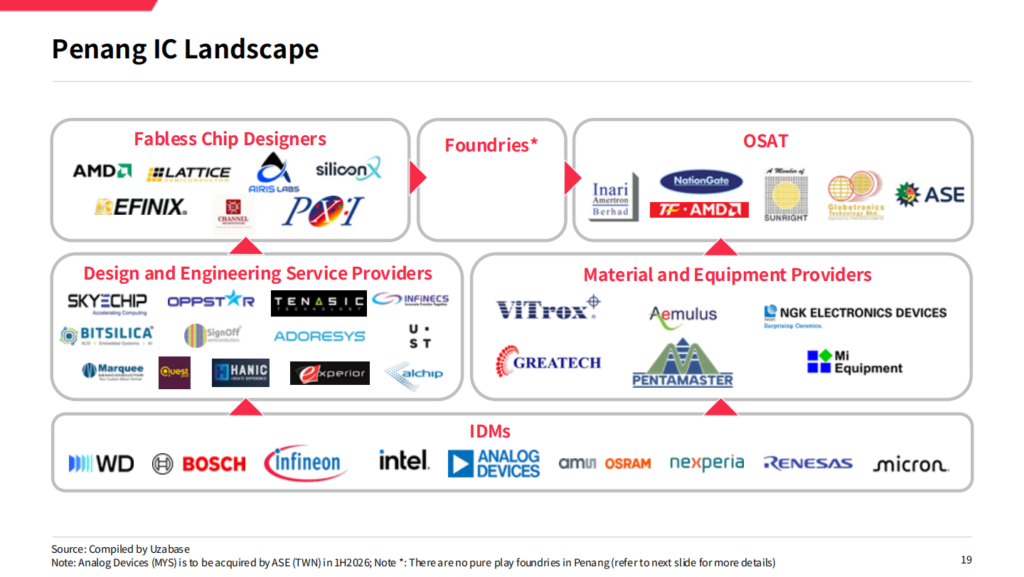

Penang: From “Eight Samurai” to Advanced Packaging and Smart Factories

Penang remains Malaysia’s most mature semiconductor cluster and a central node in the regional OSAT and advanced packaging ecosystem. Its semiconductor story began in the 1970s, when the Bayan Lepas Free Industrial Zone – Malaysia’s first FTZ – attracted an initial cohort of eight multinational manufacturers, often referred to as the “Eight Samurai”. That early wave catalysed a dense network of local suppliers, automation firms and support services that now spans the full IC value chain.

Today, Penang is a genuine “Silicon Valley of the East”: it accounts for more than 5% of global semiconductor sales and hosts three of the global top 10 semiconductor companies. Between 2015 and 2024, the state received 9% of Malaysia’s total approved manufacturing FDI, equivalent to MYR 203 billion, reflecting its status as a preferred base for global semiconductor expansion.

On the ground, the Penang semiconductor cluster is both broad and deep. There are 11 major back-end players and 148 related firms, supported by over 350 multinational corporations and more than 6,500 SMEs and technology companies across ten industrial parks and zones, including Bayan Lepas, Penang Science Park and Batu Kawan Industrial Park. The cluster covers fabless chip designers, OSAT providers, design and engineering services, materials and equipment suppliers, and IDMs.

Critically for investors, Penang is rapidly scaling advanced packaging and testing for next-generation applications such as AI, EVs, edge computing, data centres, 5G and IoT. New plants coming online from 2025 introduce advanced packaging platforms like SiP, FCCSP, FCBGA and 2.5D/3D stacked packaging, as well as wafer bumping, wafer-level packaging, flip-chip and turnkey testing. Penang is also moving toward higher-value activities via a MYR 120 million, five-year initiative to build an interconnected IC design and technology ecosystem within a 5km radius of Bayan Lepas, including an IC Design & Digital Park, a Chip Design Academy and a Silicon Research & Incubation Hub equipped with high-spec servers and EDA tools.

For private equity and M&A advisors, this advanced packaging and equipment upgrade opens several deal angles: consolidation among OSAT players, growth capital for local equipment and automation providers, and carve-outs or joint ventures as multinationals rebalance regional capacity. Using Speeda’s ASEAN company coverage, investors can screen Penang-based OSATs, IDMs and equipment suppliers by business activity, floor space, revenue scale and product focus to prioritise targets across the Malaysia semiconductor ecosystem.

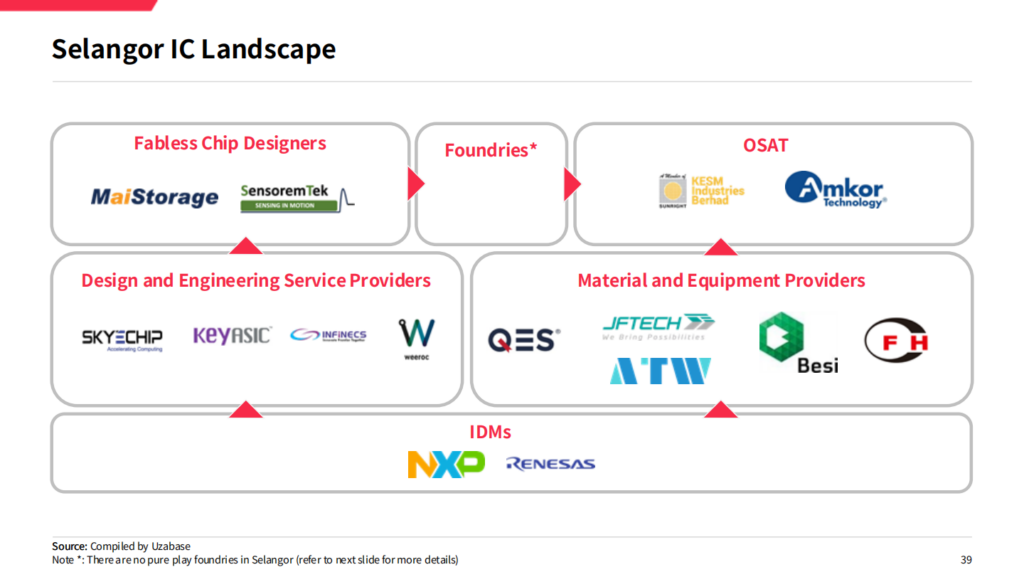

Selangor: IC Design, Power Electronics and Emerging Fabless Pipelines

If Penang is Malaysia’s established back-end and advanced packaging powerhouse, Selangor is the emerging front-end and IC design frontier. The state already generates significant manufacturing output in E&E and M&E, anchored by long-standing automotive, aerospace and data centre industries, and it hosts around 55 semiconductor-related firms across front-end, back-end and supporting activities.

Selangor’s strategy is to move up the semiconductor value chain by focusing on IC design – the highest value-adding activity – and power electronics for growth sectors such as automotive, data centres, EVs and renewable energy. Two new IC Design Parks, launched in 2024 (Puchong) and 2025 (Cyberjaya), are central to this plan. Together, they are expected to become Southeast Asia’s largest IC design hubs, focusing on electronic design automation and aiming to house at least 14–20 IC design firms and over 400 IC design engineers.

These parks offer a comprehensive package of financial support (funding, capex incentives and 10-year tax exemptions), fully subsidised EDA tools and IP/MPW services, dedicated labs and workspaces, and talent programmes such as the Global Semiconductor Exchange Program in analog and digital IC design and RISC‑V architecture. On the capital side, the Selangor Semiconductor Fund (Ehsan Capital) has been launched to back high-potential design startups.

Selangor’s IC landscape already includes early-stage fabless designers working on NAND controllers and sensor solutions, as well as design and engineering service providers that offer IP design, front-end and back-end IC design and embedded software development. A small group of OSATs and IDMs, plus a sizeable pool of local equipment providers in test, inspection and process tools, round out the cluster.

For venture investors, Selangor’s early fabless and design service companies are natural candidates for seed and Series A funding, especially where access to the IC Design Parks and their toolchains creates defensible engineering and IP capabilities. For banks and M&A advisors, the combination of incentives, available industrial land and anchored demand from automotive and data centre customers offers a pipeline of brownfield expansions, JV structures and project financing deals. Using Speeda’s database, investors can map these Selangor players by location (Puchong, Cyberjaya), activity (fabless, OSAT, equipment) and sector exposure (automotive, data centre, industrial) to build thematic portfolios in ASEAN chip supply chains.

Domestic Capital and Global IP: Dana Impak and the Arm Partnership

Malaysia’s semiconductor push is reinforced by domestic institutional capital and global technology partnerships. Khazanah Nasional’s “Dana Impak” is a MYR 6 billion investment programme targeting strategic sectors, including semiconductors and deep tech, through a combination of private equity, venture capital and direct investments. As an anchor investor, Khazanah has committed MYR 100 million to the Cambrian Fund, a PE vehicle led by Malaysian founders that focuses on Industry 4.0 themes such as machine vision, AI and robotics, and it backs a VC fund – Gobi Dana Impak Ventures – aimed at early-stage semiconductor and deep-tech startups.

On the technology side, Malaysia’s partnership with Arm Holdings is designed to compress the timeline needed to produce “Made by Malaysia” chips from 10 years to 5–7 years. Arm will provide IP licences and compute subsystems, train 10,000 IC design engineers and establish its first ASEAN office in Kuala Lumpur, under a RM1.11 billion, 10‑year programme. For IC design firms in Penang and Selangor, this improves access to cutting-edge IP and talent, and creates additional layers of potential IP licensing, JV and acquisition activity for strategic investors.

For dealmakers, the presence of a sovereign investor like Khazanah and a global IP provider like Arm lowers execution risk, creates co‑investment opportunities and supports exit scenarios ranging from strategic trade sales to public listings. Speeda’s integrated data on funds, portfolio companies and corporate partnerships allows investors to trace these capital flows across the Malaysia semiconductor ecosystem.

What This Means for PE/VC, Banks, M&A and TP Professionals

For ASEAN-focused PE/VC, Malaysia’s semiconductor strategy translates into three broad opportunity buckets: scaling and consolidation among Penang’s OSAT and equipment providers; early-stage and growth capital for Selangor’s IC design and power electronics ecosystem; and co‑investments alongside domestic institutions like Khazanah and Selangor’s state funds.

For banks and M&A advisors, the combination of RM25 billion in NSS fiscal support, new IC Design Parks and cluster-level upgrades in Penang and Selangor provides a rich pipeline of capex financing, cross-border M&A, JV structuring and capital markets mandates. For transfer pricing and tax professionals, the emergence of multi-jurisdictional design centres, IP hubs and manufacturing bases raises new questions around IP valuation, profit allocation and supply-chain pricing that require granular, transaction-level data on ASEAN semiconductor companies.

Speeda platform is built precisely for this type of use case. By combining structured financials, ownership data, industrial park mapping and value-chain linkages across Malaysia’s key clusters – from Penang’s “Silicon Valley of the East” to emerging IC design hubs in Selangor – Speeda enables deal teams to move from macro narrative to executable target lists, and from headline policy announcements to model-ready cash-flow forecasts.