Trend Reports

SEA M&A in 1Q2026: Slower Headlines, Sharper Signals for Investors

This article highlights key findings from Speeda’s report “SEA M&A 1Q2026” . If you’d like to dive deeper into deals by countries and sectors, top deals, startup financing and more findings, please submit the form to get access to the full report.

Southeast Asia’s M&A cycle has entered 2026 in a more cautious gear, but beneath the headline slowdown, the latest Speeda data shows a market quietly re-pricing risk, rotating into defensible sectors, and reshaping regional capital flows.

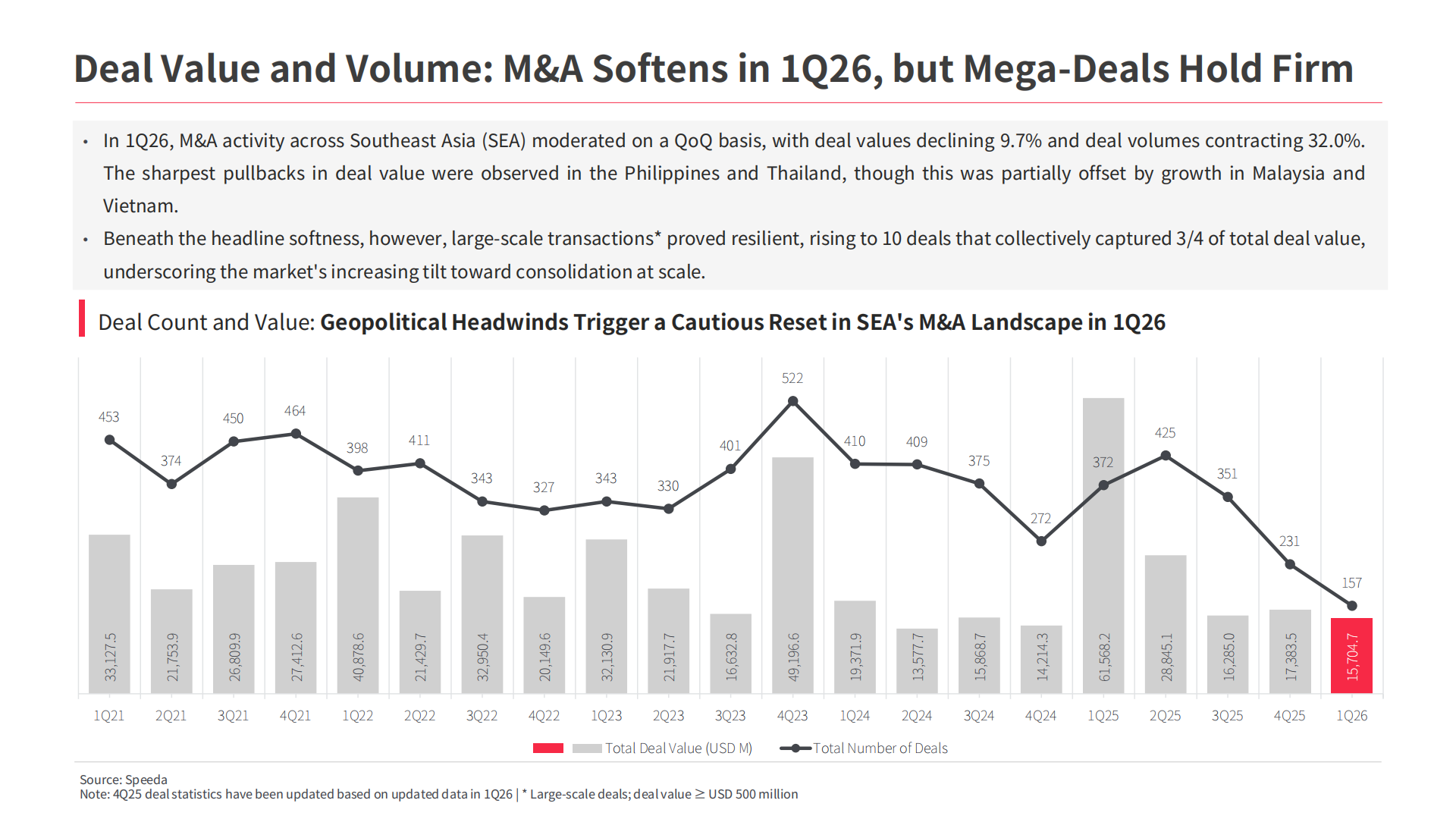

In 1Q2026, overall deal volume across Southeast Asia fell, with a noticeable drop in smaller transactions, while aggregate deal value also moderated. At the same time, large-scale and mega-deals remained resilient, indicating that investors are still willing to underwrite sizeable tickets — provided the assets are high quality and strategically critical. For investment professionals, this divergence is one of the clearest signals in the current private market environment: the bar for capital has gone up, not disappeared.

A more selective M&A cycle

Speeda’s latest SEA M&A report shows that deal activity softened across most major markets, with geopolitical tensions and stickier inflation weighing on sentiment. Yet Malaysia and Vietnam bucked this trend, posting growth in deal value as investors continued to back structurally supported stories in those markets.

For investors, this shift is reshaping deal sourcing. The pipeline is tilting away from broad-based growth bets toward targeted acquisitions in sectors where earnings quality and cash generation can withstand higher funding costs.

This is also changing how investors think about business and company valuation. The 2020–2021 multiple expansion cycle has clearly faded. Investors are now underwriting deals with stricter assumptions on working capital, margin durability, and FX/cost pass-through, driving a stronger need for granular company financial data and consistent peer benchmarks when deciding how to value a company in today’s conditions.

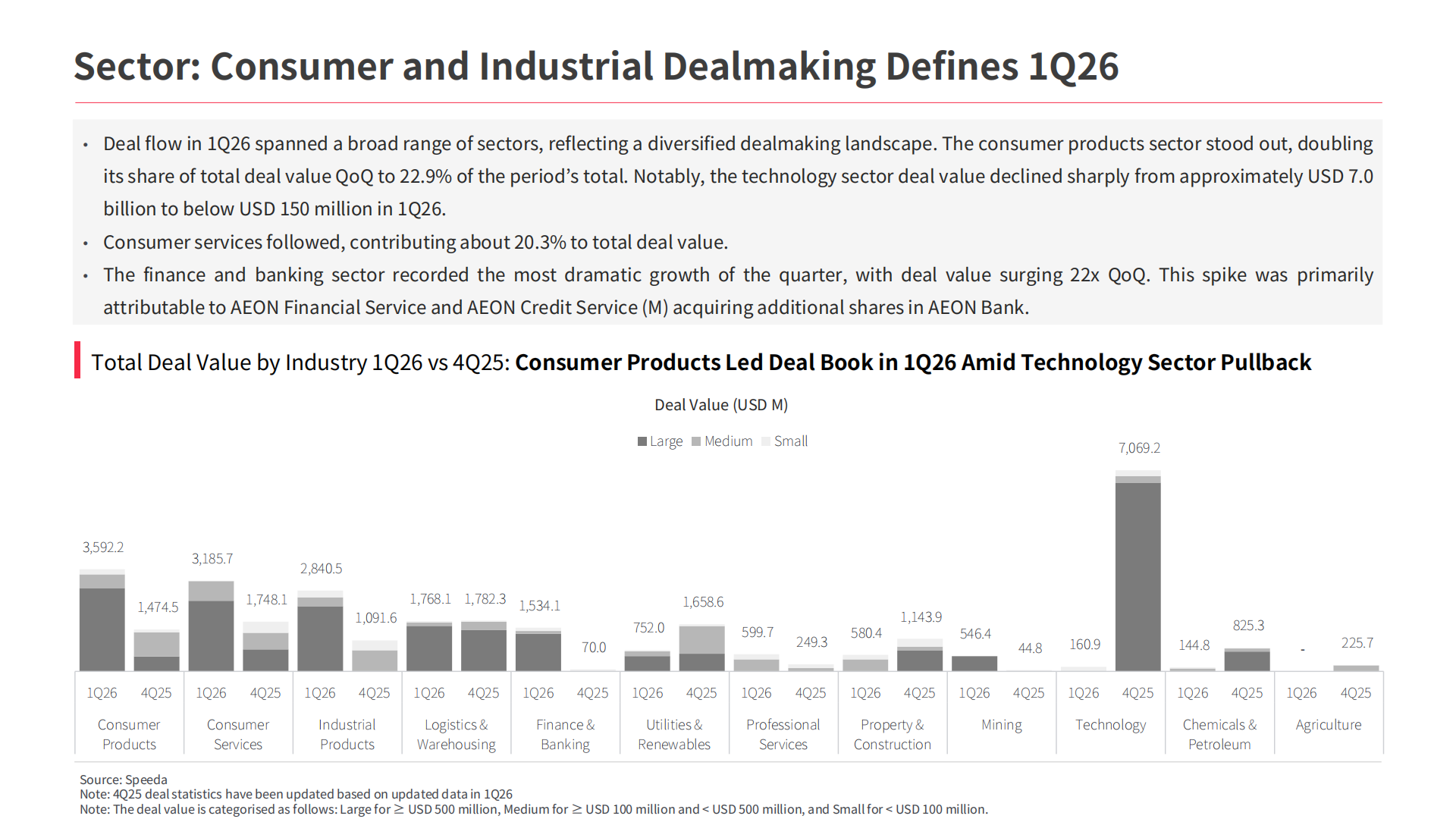

Sector rotation: consumer, industrial, and financials step forward

One of the most important insights from Speeda’s dataset is the breadth of sector participation. Consumer products and consumer services led 1Q2026 deal value, together accounting for a substantial share of regional M&A. Industrial products and logistics & warehousing also remained active, while the technology sector saw a sharp pullback in disclosed deal value compared with previous quarters.

For investment teams, this has several implications:

Consumer and services: Deals are increasingly focused on scaled platforms and resilient franchises, rather than early-stage growth stories. This is especially relevant for investors running M&A target screening across ASEAN, as the real opportunity lies in identifying regional champions with pricing power and diversified revenue.

Industrial and logistics: Supply-chain localization and portfolio optimization are creating steady deal flow around asset-light logistics, specialty industrials, and infrastructure-adjacent plays. These are areas where TP firms and sector-focused consultants can add strong value through tax, structuring, and cross-border planning.

Financials: The surge in finance and banking deal value, driven by select transactions, highlights continued interest in financial inclusion, specialty lending, and payments platforms. For deal teams using deal sourcing platforms or a company data platform, the ability to track ownership changes, licensing, and asset quality in these businesses is critical.

The sector mix also underscores a growing demand for richer industry research. As investors rotate sectors, they need to refresh their assumptions on margin structures, regulatory risk, and consolidation potential.

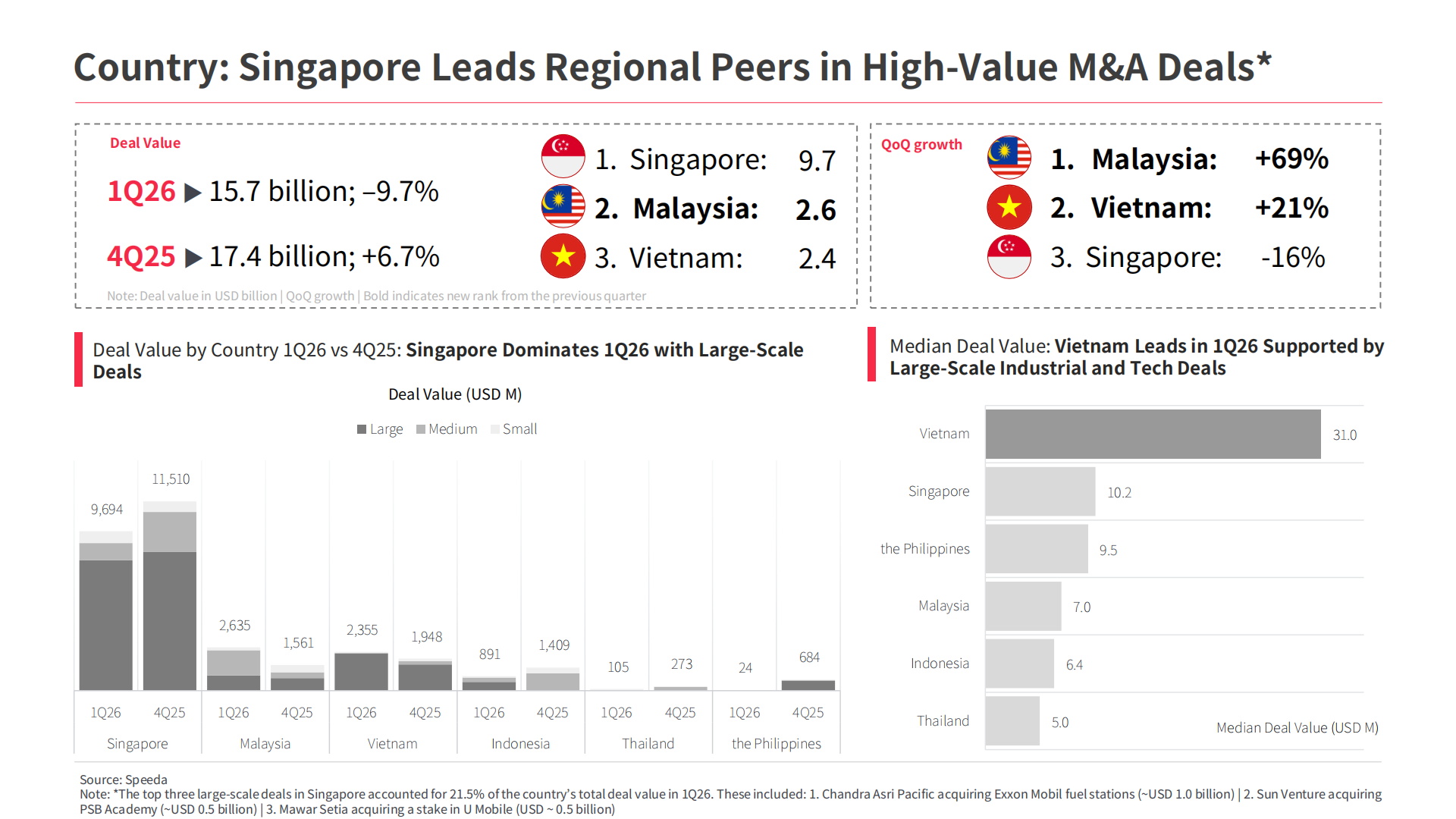

Country lenses: Singapore, Malaysia, Vietnam in focus

Singapore remains the region’s core hub for capital, transaction structuring, and headquarters functions. Many of 1Q2026’s largest deals involve Singapore either as buyer, seller, or domicile, reinforcing the city-state’s role in regional business investment Singapore and business opportunities in Singapore.

Malaysia, meanwhile, saw a notable jump in deal value, propelled by consumer services mega-deals and healthcare transactions. For users focused on company check Malaysia, company profile, or malaysia company search, this quarter’s activity highlights the importance of understanding domestic champions and their regional expansion strategies, as well as how corporate restructurings may create new opportunities.

Vietnam continues to attract attention from both strategic and financial investors looking at foreign direct investment in Vietnam and foreign investment in Vietnam. Industrial and tech-related transactions underscore Vietnam’s role in regional manufacturing, electronics, and emerging digital ecosystems. This is where reliable business profile and company data—particularly for unlisted firms—can provide a competitive edge in deal sourcing venture capital and mid-market buyouts.

What this means for investment professionals:

A slower headline M&A market coupled with resilient large deals is a classic environment where information advantages matter more. The key shifts visible in Speeda’s report suggest that:

Quality beats quantity in deal flow: Fewer transactions, but more emphasis on strategic fit and robust fundamentals, increase the premium on accurate company data and company financial data when evaluating opportunities.

Private market transparency is a differentiator: With public-market signals less representative of where growth is happening, investors and advisory teams need reliable access to Asia-focused company data for screening, company profile building, and comparative business valuation work.

Integrated research and data are becoming standard: As sector rotations accelerate, teams increasingly expect to move from high-level industry research into target-level diligence on the same platform, including business valuation, ownership, and peer benchmarks.

For investors and advisory teams, this environment rewards those who can combine proprietary investment theses with robust financial data and structured company data to move quickly when high-quality assets come to market.

How Speeda can support your next move

Speeda’s latest M&A report is built mostly on Speeda data and insights, covering:

Quarterly trends in deal value and volume across ASEAN

Sector-level breakdowns, median deal sizes, and valuation patterns

Country snapshots for Singapore, Malaysia, Vietnam, Indonesia, Thailand, and the Philippines, etc.

Start-up and growth-stage transaction dynamics, including the growing role of private equity

To explore how Speeda can help you in Asia market, consult us for more Asia private company data and industry insights.

Our team will also be hosting a webinar on May 8, where the report’s editor will walk through the 1Q2026 findings in detail and discuss what they mean for your investment pipeline and client mandates. To join the webinar and read full report, please register here.

Thank you for your submission!

We will send an email with the download link to access the report shortly.

Follow our Linkedin Page !

Our latest updates on

ASEAN reports and webinars are posted here.