Trend Reports

Southeast Asia’s Data Centre Boom: What Investors and Advisors Should Watch

This article outlines key trends in Southeast Asia’s data center market. To turn these insights into a concrete target list or peer set, you can request a demo and customized company list here.

Capacity Unleashed: Why Southeast Asia’s Data Centre Market is Gaining Momentum

Southeast Asia’s data center market is moving into a new phase of growth. What was once concentrated in Singapore is now expanding across the region, supported by stronger digital demand, tighter data localization rules, and growing interest in AI-ready infrastructure.

For investors and advisors tracking infrastructure, technology and cross-border opportunities in Asia, the key question is where growth is building fastest, what is driving it, and how the market map is changing.

A fast-growing market with room to scale

The region is expected to see the fastest data center capacity growth globally, with 35% CAGR over 2023–2028, compared with 15% globally, according to Speeda report.

That growth starts from a relatively low base, which is part of the opportunity. Southeast Asia still has fewer existing data centers than more mature markets, but the pipeline is expanding quickly as operators and investors build out regional capacity.

Why demand is rising

First, data sovereignty and localization rules are pushing more data to be stored and processed domestically. Malaysia, Vietnam and Indonesia are all tightening or updating their regulatory frameworks, increasing the need for local infrastructure.

Second, the region’s digital economy continues to expand rapidly. The report notes that Southeast Asia’s e-commerce market is projected to grow at 21% CAGR over 2025–2034, while the fintech market is projected to grow at 11% CAGR over 2025–2033. These sectors rely on low-latency, reliable infrastructure, which raises demand for in-region data center capacity.

Third, 5G adoption, IoT applications and AI workloads are changing what kind of infrastructure is needed. Edge data centres are becoming more important for real-time processing, while AI applications require much higher rack density and more advanced cooling than traditional facilities.

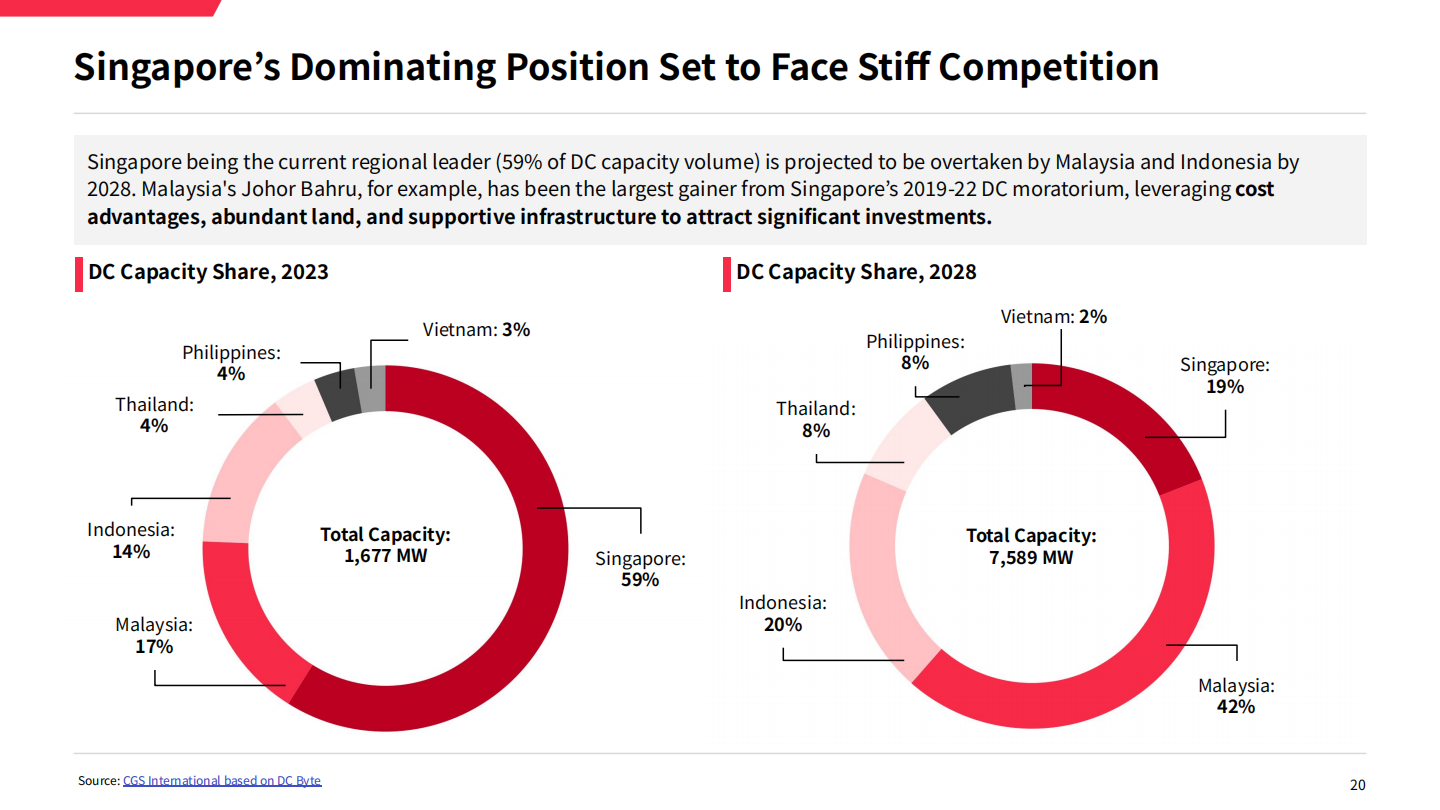

Singapore still leads, but the balance is shifting

Singapore remains the region’s leading data center hub today. It accounts for 59% of Southeast Asia’s live supply, and its facilities have the highest average megawatt capacity in the region. This reflects its strong connectivity, policy support and mature ecosystem.

But the next stage of growth is unlikely to be concentrated in Singapore alone. Speeda report shows that by 2028, Singapore’s share of regional data center capacity is projected to fall to 19%, while Malaysia is projected to rise to 42% and Indonesia to 20%. In absolute terms, total regional capacity is projected to increase from 1,677 MW in 2023 to 7,589 MW in 2028.

That shift is also visible in country growth rates. Between 2023 and 2028, the report projects capacity CAGR of 63% for Malaysia, 45% for Indonesia, 58% for Thailand, 59% for the Philippines, 25% for Vietnam, and 8% for Singapore.

For market participants, this suggests a more distributed regional model: Singapore remains the premium hub, while Malaysia and Indonesia are becoming increasingly important for large-scale expansion.

Why Malaysia and Indonesia are gaining ground

The report points to a practical set of advantages behind this shift. Malaysia and Indonesia offer lower set-up and operating costs, more abundant land, and supportive infrastructure and policy conditions. These factors make them attractive alternatives for space-intensive and cost-sensitive projects.

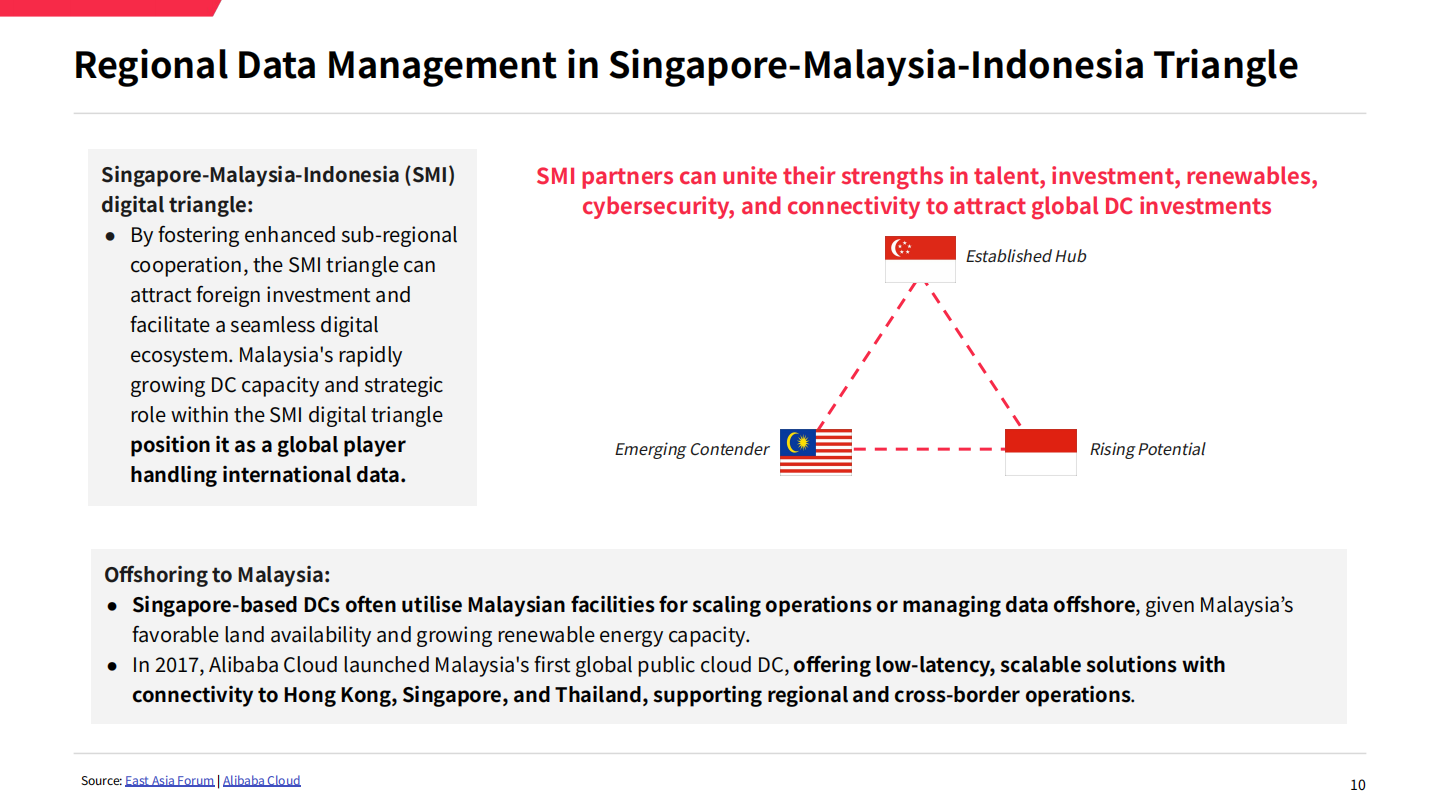

Malaysia stands out in particular. The report notes that it is the only Southeast Asian market that effectively meets both reliable power and abundant water conditions, which are critical for large-scale data center development. It also highlights Malaysia’s role in the Singapore-Malaysia-Indonesia (SMI) digital triangle, where regional cooperation can support investment and enable a more seamless digital ecosystem.

The report’s actionable view is clear: use Malaysia and Indonesia for space-intensive, hyperscale operations, while reserving Singapore for premium, high-density AI infrastructure and strategic data management.

Connectivity and resilience matter

Market growth is not only about demand. Supply-side conditions also shape where data center capacity can be built efficiently.

The report highlights several enabling factors across Southeast Asia: expanding bandwidth capacity, strong submarine cable infrastructure, and the region’s relatively neutral geopolitical position. As of 2025, Indonesia, Singapore and Malaysia had the highest number of submarine cable systems in the region, and upcoming projects are expected to strengthen connectivity further.

At the same time, the report is clear about constraints. Uneven electricity reliability, water stress and exposure to natural disasters remain important considerations in some Southeast Asian markets. These are not side issues—they directly affect long-term asset performance, operating resilience and site attractiveness.

Green data centers are becoming more important

The growth story is also being shaped by sustainability requirements. Speeda report highlights opportunities in energy-efficient design, eco-efficient cooling and renewable energy integration.

From market insight to deal work

For investors, advisors and consulting teams, the real value of this theme lies in turning market insight into action.

Speeda supports your workflow by:

Screen targets and peers across Asia with local private company and industry mapping data.

Analyze deal activity and valuation benchmarks using transaction data and valuation multiples.

Support due diligence with financial data, industry reports and expert network input.

To see how deal teams use Speeda in practice, please click here to explore our client story with Nihon M&A Center Inc.

And if you want to assess this theme in your own focus markets, apply for a free trial in below. You could ask for a customized list of relevant companies, peers or targets based on your investment priorities, and also talk to us for local expert network services.