Industry Reports

Thailand Healthcare’s High Growth Segments: Playbook for Investors and Advisors

Thailand’s healthcare sector is evolving into a high-value ecosystem, anchored by medical tourism and an aging population. This piece breaks down Thailand’s healthcare ecosystem, highlighting practical investment windows across medical devices, residential aged care and private hospitals.

To turn these insights into a concrete target list, you can request a demo and customized company list here.

Three Highlighted Segments for Deal Sourcing

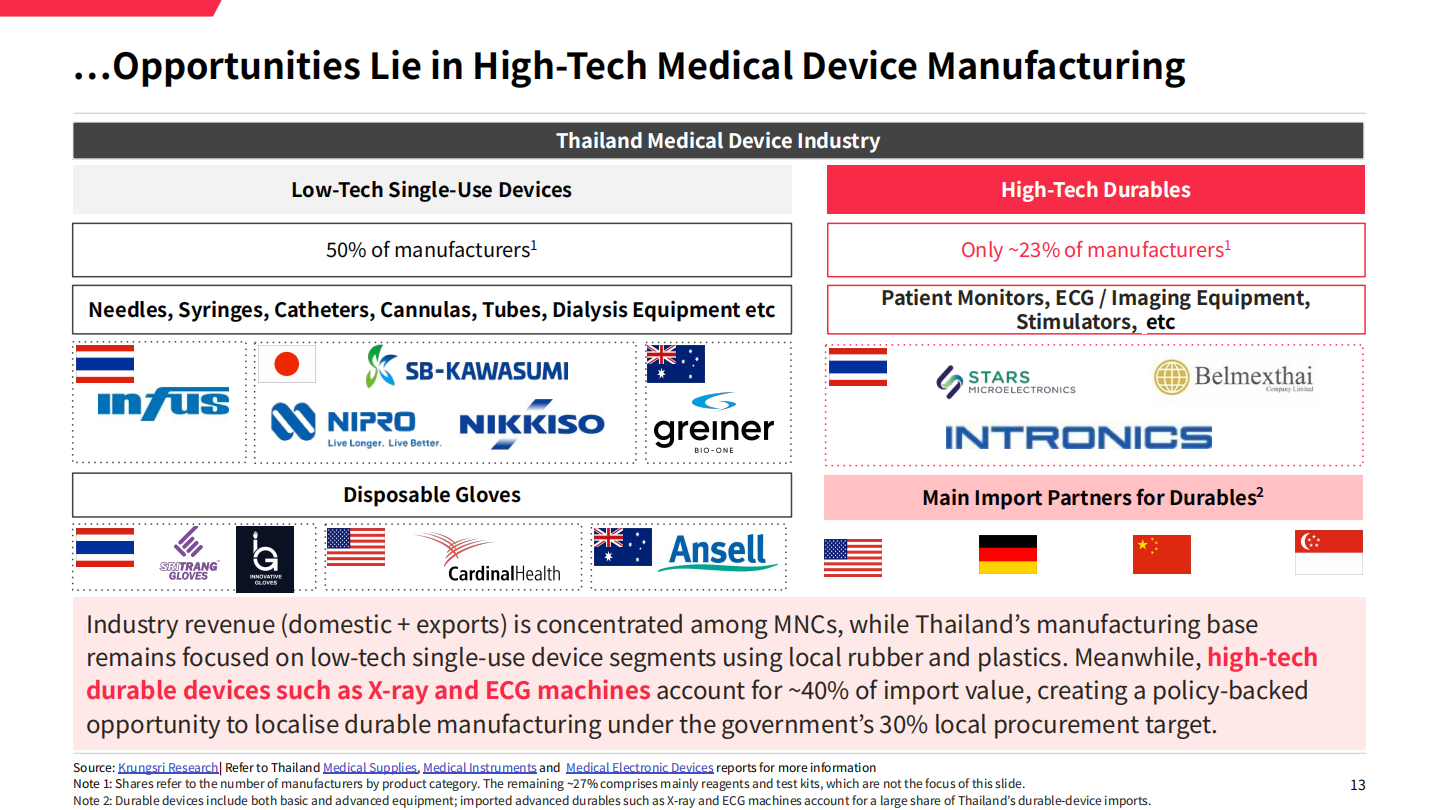

1. Medical Devices: Localization Upgrade Play Backed by BOI Incentives

Market size: ~USD 2bn in 2024, with an indicative 6% CAGR forecast for 2024–2029.

Thailand’s medical device industry combines devices and equipment and is broadly categorized into single‑use devices, durable devices and reagents or test kits. Production and exports are heavily dominated by lower‑tech single‑use consumables such as syringes and latex gloves, while higher‑value durable devices like imaging and monitoring equipment account for a large share of imports, around 40% of durable‑device import value. This gap between local single‑use production and imported durables creates a localization opportunity, especially for investors focused on manufacturing upgrade paths.

The Thailand Board of Investment (BOI) offers tiered tax incentives that significantly improve project economics for qualifying manufacturers. High‑risk, high‑tech A2 medical device projects (e.g. advanced imaging, pacemakers) can obtain 8 years of 100% corporate income tax exemption followed by a further 5 years at 50% reduction, adding up to as much as 13 years of tax relief. A3 and A4 categories (general devices and certain fabrics, masks and parts) receive shorter exemption periods but still benefit from extended tax support.

Auto component suppliers represent potential acquisition and partnership candidates. Local metal, plastic and rubber manufacturers are already pivoting into rehab gear, adjustable patient beds and mobility aids via hybrid manufacturing models, avoiding full operational overhauls. Key diligence risks center on TFDA regulatory timelines (250–300 day review windows for Class II–IV devices) and steep ISO 13485 compliance switching costs, though the TFDA-HSA reliance scheme cuts approval lead times to 60–150 days for Singapore-certified hardware.

2. Residential Aged Care: Low‑Base Growth with Partnership‑Driven Entry

Market size: about USD 74mn in 2024, with a high 26% CAGR forecast through 2033 from a low current base.

Residential care is one of Thailand’s most under‑served healthcare subsegments. As of 2024, seniors aged 65 account for more than 11 million people, roughly 16% of the population, yet formal residential care capacity stands at only around 20,000 beds. This translates to approximately 2 beds per 1,000 elderly, significantly below peer benchmarks such as Singapore’s 27 beds per 1,000 seniors and a realistic emerging‑market parity floor of 10–15 beds per 1,000 elderly.

Demographic trends reinforce demand. Thailand is expected to become a super‑aged society by 2033, with about 28% of the population aged 60 or above, while shrinking multi‑generational households erode traditional family‑based elder care.

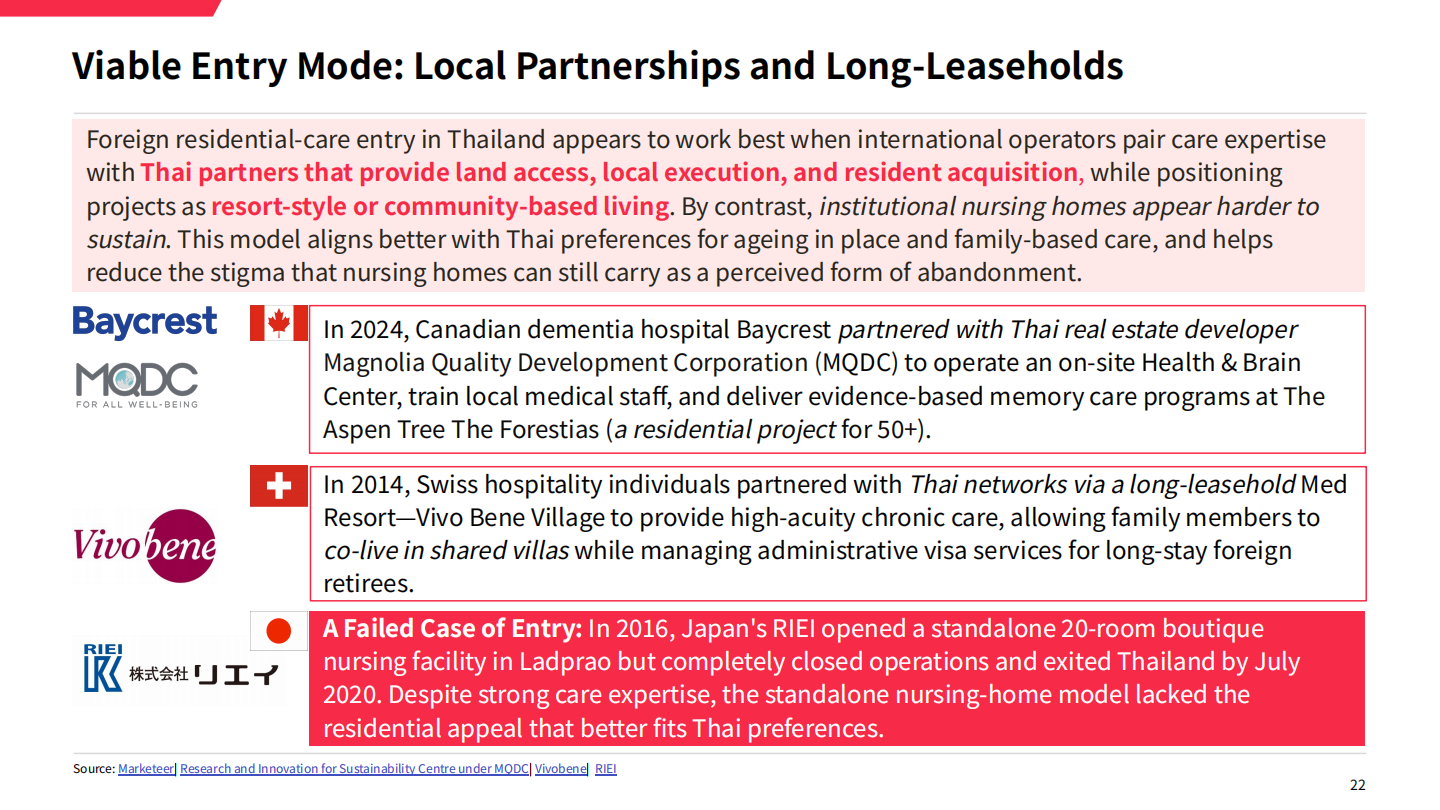

Regulatory constraints dictate deal structure: foreign investors are capped at 49% equity ownership under the Foreign Business Act and cannot own land outright, requiring 30-year long leaseholds paired with local real estate or hospital group JVs. Standalone boutique nursing homes have proven harder to sustain, while integrated resort-style senior townships (such as MQDC’s partnership with Canadian dementia specialist Baycrest) have delivered more stable occupancy and lower social stigma. Operational value levers for PE include AI monitoring robotics and 4D radar fall-detection systems, which cut caregiver workloads by 36–48% to offset a projected 250,000 domestic care worker shortage by 2037.

3. Private Hospitals: Medical Tourism and Specialty‑Care Alliances

3. Private Hospitals: Medical Tourism and Specialty‑Care Alliances

Market size: about USD 10bn in 2025, with an indicative 6% CAGR forecast for 2025–2030.

Thailand’s positioning as ASEAN’s leading medical hub underpins private hospital upside, with treatment costs 50–75% cheaper than US and Singapore equivalents, plus 60+ JCI-accredited facilities and a 90-day medical visa for long-stay international patients. Domestic industry fragmentation creates consolidation opportunities: Thailand hosts 370+ private hospitals and 26,000 clinics, with large listed chains (BDMS, Bumrungrad, Thonburi Healthcare) capturing much of the revenue while many small independent operators focus on routine care. These major groups are actively expanding wellness resort extensions and cross‑border joint ventures.

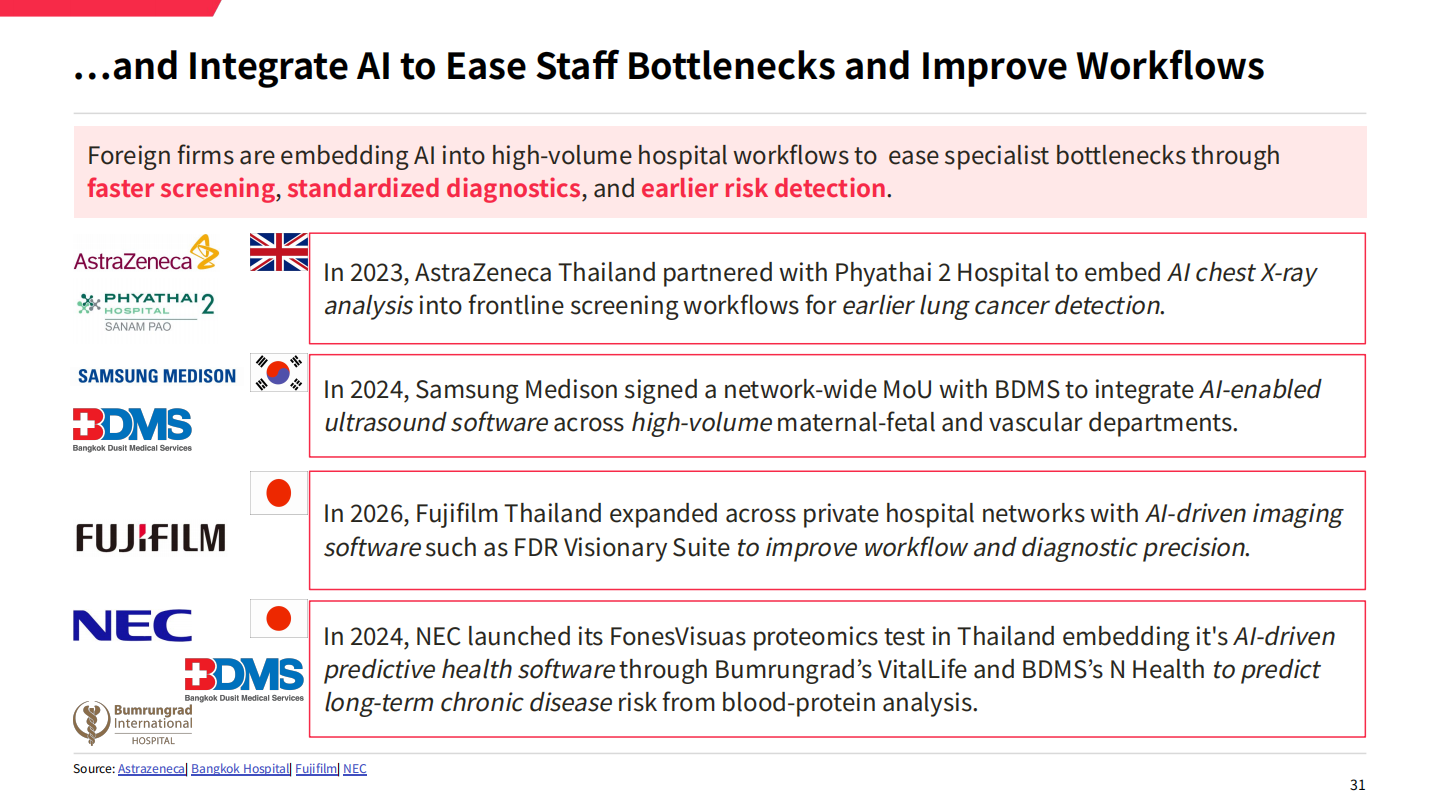

Foreign deal flow centers on specialty clinical partnerships, not full hospital acquisitions. Recent landmark tie-ups include Samitivej Hospital’s liver transplant collaboration with South Korea’s Asan Medical Center and Bumrungrad’s genomic medicine MoU with BGI Group. AI diagnostic integration presents a clear operational uplift play—Samsung Medison, Fujifilm and AstraZeneca have all deployed AI imaging tools across major networks to ease physician staffing bottlenecks. Key margin headwinds include state price controls on essential medical services and rising competition from Malaysia’s low-cost medical travel offerings.

Takeaways for Investors and Advisors

Takeaways for Investors and Advisors

Across these three subsegments, partnership models are more common than full foreign control, and that reality should be a central part of deal planning:

- Medical devices: Joint ventures with local automotive or industrial manufacturers and hybrid manufacturing structures can be more practical than greenfield durable‑device plants, especially when leveraging BOI tax incentives and local procurement mandates.

- Residential care: Tie‑ups with Thai real estate developers or hospital networks help secure land access, clinical referral pipelines and local execution, while working within foreign ownership caps and leasehold rules.

- Private hospitals: Minority specialty‑care alliances, AI and digital‑health integrations and service‑line partnerships often face fewer regulatory and operational frictions than full asset acquisitions.

Stress‑testing downside scenarios is also important: TFDA approval delays and regulatory complexity in med‑tech, persistent geriatric labour shortages constraining residential care expansion, and intensifying regional medical tourism competition squeezing private hospital margins.

How Speeda Supports Thailand Healthcare Deal Workflows

Speeda provides tools that connect this kind of sector insight to company‑level intelligence:

- Screen private manufacturers, residential care operators and private clinics/hospitals with granular local industry mapping.

- Access healthcare transaction data and sector information to support valuation and benchmarking.

- Run regulatory and demographic checks through targeted expert interviews with local healthcare operators and advisors.

If you’re exploring private market data in your focus markets, apply for a free trial below to request a customized list of relevant companies based on your investment priorities, and talk to us about local expert network support.